The circular economy – time for consistency

With upcoming changes in European requirements under CSRD/ESRS, you must consider how you are a part of the circular economy. But what is it? What can you do to be integral to it? And why should you care?

Introduction

The concept of a circular economy has existed for a while but has evolved. With upcoming requirements to report on it, has the time arrived to “gather around” a standardised definition? What exactly is the circular economy? What can your company do to make the most of it? And what will you have to report on when the regulations arrive?

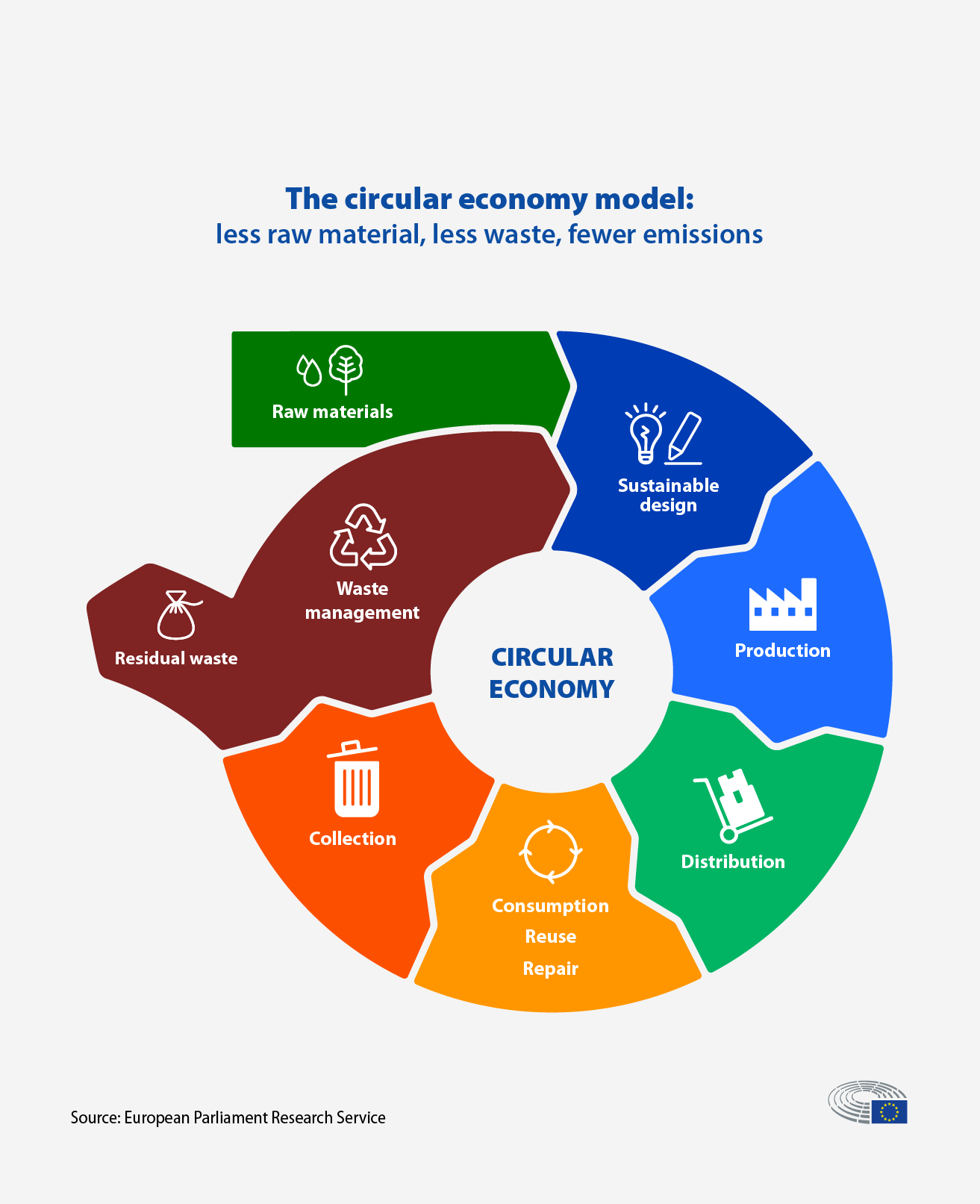

Defining the circular economy

The principles behind a circular economy are an extension of the “reduce, reuse, recycle” mantra that many UK readers will be familiar with, but at the business level rather than the household level. In the upcoming Corporate Sustainability Reporting Directive (CSRD) and European Sustainability Reporting Standards (ESRS) that many European-facing companies will have to report on, a circular economy is:

“An economic system in which the value of products, materials and other resources in the economy is maintained for as long as possible, enhancing their efficient use in production and consumption, thereby reducing the environmental impact of their use, minimising waste and the release of hazardous substances at all stages of their life cycle, including through the application of the waste hierarchy.”

Why you should care

The reason to care is two-fold. Firstly, you likely must from a reporting point-of-view, and secondly, by committing to improving the circular economy, your business is more likely to open itself up to more long-term value-creation opportunities.

Opportunities for business beyond the reporting requirements

Circular opportunities play into the wider responsibility of business as global citizens and help you align with three big expectations we are witnessing: “restoring trust in business”, “addressing the authenticity gap”, and “balancing long-term outcomes vs short-term performance”.

When communicated correctly, companies that push themselves to be more integral to the circular economy will be perceived as authentic and trustworthy. By tackling long-term issues, companies will attract wider stakeholder support, including investors, and minimise the number and impact of potential risks.

The circular economy is such a broad concept that deciding how to approach it can be challenging. Focusing on certain activities, or parts of the life cycle, is a sensible approach. In its “Mapping the benefits of a circular economy” survey, McKinsey found that every industry could improve its financial performance and reduce costs by pursuing six activities. They are:

1. Regeneration – shifting to renewable energy and materials;

2. Sharing – prolonging the lifespan of products through maintenance and design;

3. Optimisation – improving product efficiency and removing waste from supply chains;

4. Looping – keeping components and materials in closed loops through remanufacturing and recycling;

5. Virtualising – delivering goods and services virtually; and

6. Exchanging – replacing old materials with advanced renewable ones or applying new technologies.

Every industry could improve in at least three activities, improve performance, and affect the bottom line. Deciding how many you tackle depends on your appetite and the nature of your business.

Upcoming reporting requirements

Under the upcoming CSRD ESRS requirements, companies will have to report against six standards as a part of ESRS E5. This will improve transparency and enable investors to compare companies more readily, improving investor confidence.

E5-1

Policies related to resource use and circular economy.

Show your organisation’s circular economy-related policies.

E5-2

Actions and resources related to resource use and circular economy.

Explain your organisation’s circular economy-related actions and the resources allocated to conduct these actions.

E5-3

Targets related to resource use and circular economy.

Report on your organisation’s resource use and circular economy-related targets.

E5-4

Resource inflows.

To understand the resources used in your operations and value chain, provide insights into your organisation’s material resource inflows.

E5-5

Resource outflows.

Provide insights into your organisation’s material resource outflows, including waste and the contribution to a circular economy, resulting from designing circular operations and production, the actual recirculation of products and materials, and waste management strategies.

E5-6

Anticipated financial effects from material resource use and circular economy-related impacts, risks and opportunities.

Show the risks and opportunities you face as a result of resource use and circular economy-related impacts.

The regulations are extensive from both data-gathering and management oversight perspectives. The requirements will likely result in companies adapting their operations and focussing on developing some of the six activities mentioned earlier.

Conclusion

As requirements come in that companies will have to report on, the circular economy is moving from being an idealistic concept to being integral to your value creation model, business strategy, and operations. This affects your reporting narrative and data disclosures. Are you ready?

If you’d like to discuss this, or any other subject, please get in touch with George Luck, Consultant at george@gather.london

We’d love to know what you think.